Look, $150K is a haul of money–even in today’s dollars where we’ve seen a lot of inflation across the board going into the early 2020’s

Here’s the thing–at that income level you can either be barely scraping by–or saving 70% of your income.

What really matters is your savings rate. How much are you spending?

Lifestyle Creep at $150K

Look, it normally takes awhile for folks to build up in their career to get to the point where they are bringing in $150K per year.

Along the road–a lot of people get tempted into increasing their lifestyle costs as their income slowly ramps up.

Getting incremental raises over the years about matches the lifestyle ramp up–and next thing you know–you’re making $150,000 per year and you’re spending all your money on a huge, fancy house, multiple new cars, and private school for the kids.

In order for $150K to be enough, and more than enough to build insane amounts of wealth–you need to fight against this lifestyle creep while getting to the $150K level.

Let’s get that out of the way before we dissect how good a salary $150,000 can be, and my strategy for how I would spend and invest this amount of money per year to live a fulfilling life.

$150K Is Good in Some Cities, Not as Much in Others

There’s a huge difference between $150K in Tulsa, OK and Los Angeles, CA. The difference is mainly two things:

- Costs for housing

- Taxes in income

If you’re living in America, those will be the two biggest factors in how far $150K can stretch.

The crazy thing these days is that you can sometimes get a high salary, but live in a low-cost area with a remote job (aka geo-arbitrage).

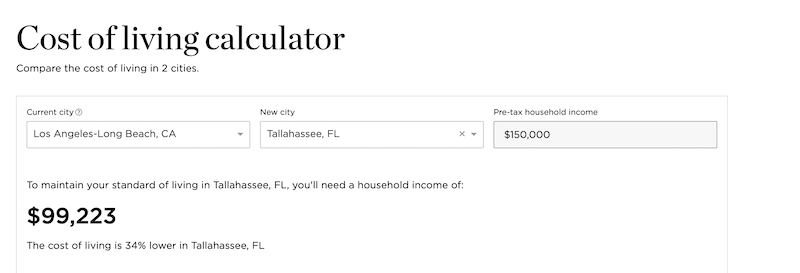

Let’s take an example of how powerful this can be using a cost of living calculator.

That same $150K in Los Angeles buys the same lifestyle in Tallahassee for $99K. That means you can change nothing about your lifestyle, and you’ve magically create a $50,000 per year margin just by changing your location.

So location is huge and that’s the main driver that dictates how “rich” you’ll feel (and actually be) if you live in a low cost of living city vs. a high one.

Saving – The Magic of Math and Quality of Life on $150,000 per Year

When you can generate a lot more income than your spending every year–it won’t take very long at all to stack up an absolute bag of cash.

When I was early in my career (and had zero knowledge about finances)–I thought that in order to have a net worth of $1M, that I’d have to straight up save $1M in a bank account, in cash.

I literally had no idea that people could invest and that the capital could grow on it’s own without me having to go out and work for every dollar at some job.

The good news is, it turns out there are things called investments that can grow capital on it’s own!

How you go about doing this is an open book. Some folks like real estate, some others prefer passive index funds, some prefer other vehicles like small businesses, franchises or all sorts of other investment vehicles.

How you get to that point, though, is saving so you can invest in the first place.

Can you live below the “standards” of your friends making $150K?

The key to making your money work for you is actually having something left over after you pay your bills every month.

That means living in a more modest house or apartment and driving a crappier car than all of your friends.

It probably means not blowing 20 grand on a European vacation–or splurging at restaurants 4 times per week.

If you can find a way to live on around $50,000 per year, and your take-home pay is somewhere around $120K per year after taxes–you’ll have an extra $70K per year to invest in things that work for you and compound over time.

Here’s the crazy thing–70 grand per year adds up to A LOT more money than you think over time.

Let’s plug 70 grand per year into a compound interest calculator and see how quickly $150K per year can make you rich.

Assuming your investments earn an average of 7% per year and you are starting at 0–within 10 years you’ll go from nothing to around $1M in assets in 10 years.

Pretty awesome stuff!

Can you really live a good life saving that much of your $150K salary

The short answer to this is yes–it turns out you can crush it, have fun, and still save loads of money.

Here’s a few key areas that you can get right-and some areas you can splurge and still come out way ahead.

Here are the killer areas where most people lock themselves into bills that drain them of their cash every month:

- Getting a huge mortgage payment or underestimating the cost of house maintenance

- Consistently buying new cars on payments, and flipping them for a new car as soon as they payments are done (car tread-milling)

- Huge, splashy purchases made with credit cards instead of saving

Let’s start with housing because it’s the number 1 thing people get caught with.

Housing

Ok–so just about everyone I know in their 30’s or older all want to be a homeowner. Here in America, homeownership is a way of life and a right of passage. We’re a country that prides itself on owning things–especially property.

Here’s the thing–the argument that owning a home is “cheaper” than renting is not always true–you need to factor in pretty high maintenance costs.

Most people have no idea how much a roof costs–how much an HVAC unit costs (or what that even is). Do you know what it costs to repair a fence, or re-paint the outside of a house.

It’s a lot. And odds are–you’re not factoring it into your budget at all. Things might be good for a few months, or even a few years–and then BAM, you get hit with a 10 or 20K bill all at once. Where you budgeting for that amount every month–or were you splurging it away?

You need to factor in maintenance when you decide what mortgage payment you can “afford”. You need to factor in at least 1% of the value of the house that you set aside every year in case you need it (and you will, and it will happen at the worse possible time).

At $150K per year salary with a goal of living on around $50K per year–you’ll want to keep your housing cost including maintenance at no more than $25,000 per year–mortgage payment, taxes, insurance and a maintenance budget. That’s over 2K per month and you ought to be able to manage that in a lower cost of living area–even in 2022. And if you can’t keep saving for a larger down payment so you own more of the house without borrowing.

The new car treadmill

I like to call people that buy a new car, pay it off over 5 years, then immediately run to get another car again as folks that are New Car Treadmillers.

Transportation is often the second largest budget item for most households–but if you want to start seriously building wealth on a $150K income–you’ll want to drive your transportation costs to below what your food costs are.

That means that you’ll need to get off the treadmill for good and actually own the cars you are driving around instead of renting them from the bank constantly.

The typical car payment in America today is damn near $700 per month. Assuming you actually own your car–that would be an additional $700 per month that you’d have in your pocket every month–and a nice notch lower for your overall costs.

Driving around low cost, fuel efficient, reliable older cars that are paid for is absolutely crucial for living on $50K or less out of your $150K per year salary.

Once you get off the treadmill, you’ll never want to get off of it. The key will be to continue saving that extra money every month–and at some point buying the next car in cash when that day comes.

$700 per month turns into $10K in 14 months. In 24 months you’ll have a whopping $20K in extra cash. Let that sink in. In 24 months, you could buy another car with the cash, easily–and it would be a really nice, reliable ride as well.

The problem is most people never get off the treadmill and keep buying insanely priced cars on huge monthly payments. Avoid this!

splashy splurging with credit cards

Using plastic to buy those splurgy purchases take the pain and discipline out of the equation.

If you had to scrape together a couple thousand bucks for that new guitar instead of just swiping the plastic–you might think twice about it.

While I’m more a fan of attacking the high monthly recurring bills in a budget–these big one-offs can be a problem for people–especially when they are bringing in a huge $150K salary.

It will tempting to swipe and just not worry about it–but come on, let’s be disciplined about it and avoid using credit cards for these massive purchases. It’s going to add up to a lot more than you think and keeping that a big credit card balance adds another huge monthly payment to your bills.

Living The Good Life on $150K

If you can manage to get your income to $150,000 per year salary–congrats. You are killing it! Most people around the world would only dream of brining in that sort of income–and you’re actually doing it.

Now, exercise discipline and be smart about how you allocate that income.

Think about your financial life like a business. What’s your profit and loss statement for your household?

If you can get that part of your life right–then eventually that income will start to work for you in a major way.

If you’ve found your way to that high of an income, you’re probably a hard worker–make sure you’re keeping as much of it as you can so it can finally start working for you one day.

Onwards and upwards!