This blog should not be taken as financial advice–it’s written purely for entertainment purposes. Sit back and enjoy! Consult a financial advisor (not me) for all financial advice.

Ok folks, I’ve seen the number $500K thrown around a lot when it comes to the idea of “coast fire” — stopping the aggressive saving and letting the money compound on it’s own until the “normal” retirement age which is somewhere around 65.

The idea is, if you can save aggressively earlier in your life, then you can loosen up a little bit, spend your income more freely (or work less) and let the nest egg compound for you.

Coast Fire Math – Expenses

Estimating your expenses are everything when it comes to figuring out what your coast fire number needs to be.

If you’re frugally living on, say $40K per year, you’ll be able to cover your living expenses with a safe withdrawal rate of 4% when you hit 1M in assets.

Assuming you’re invested in an index portfolio that tracks a broad range of stocks (like the SP 500), then you’re looking at around 10 years of letting the $500K grow until it hits the magic 1M number.

Expense are a huge lever in the FIRE equation. The more you can reduce your spending, the less you’ll need in assets to cover your bases.

Your Age at Coast Fire

Your age has a lot to do with what your “Coast Fire” number needs to be. The younger you are, the more theoretical time you’ll have to let your money compound into retirement.

$100K in assets at 25 holds a lot more compounding power than $100K at 50.

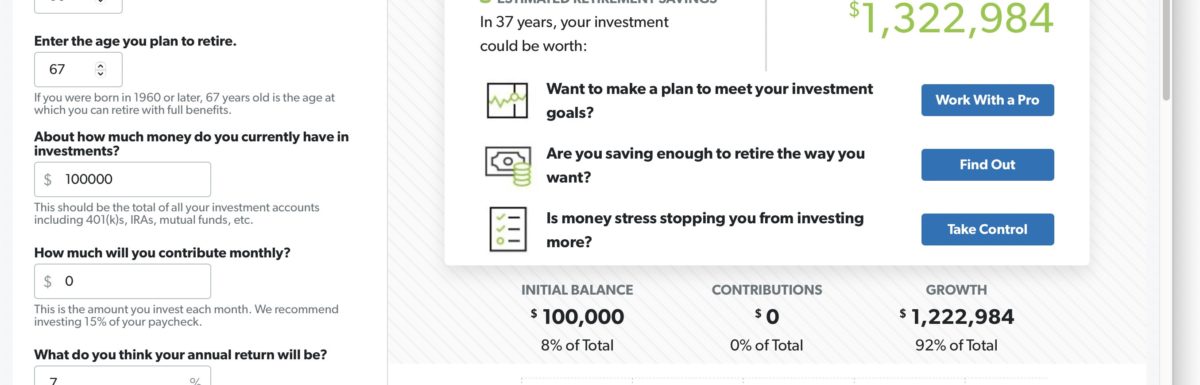

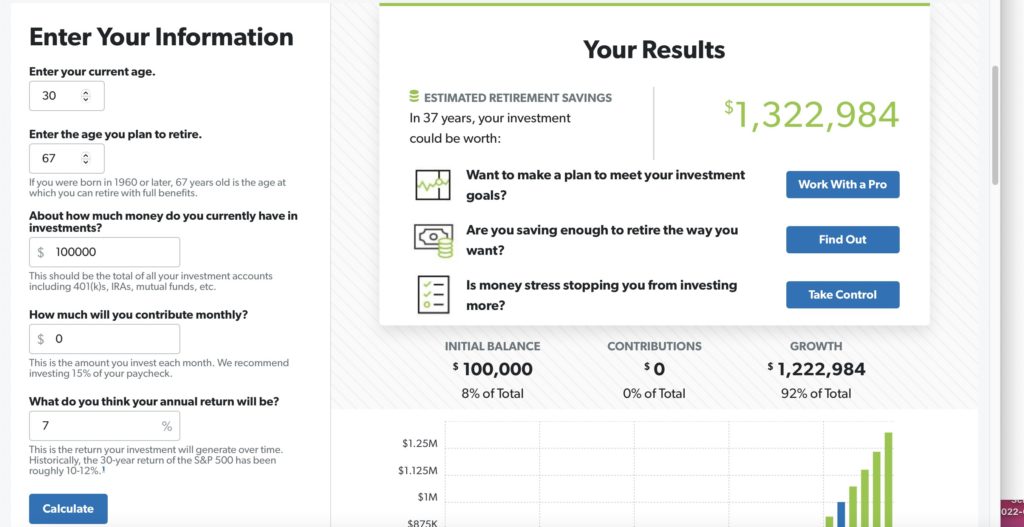

Let’s see how this works using our handy investment calculator:

In this situation–the 30 year old is compounding 7% for 37 years–which turns the initial $100K into a whopping 1.3M. That’s an insane amount of growth.

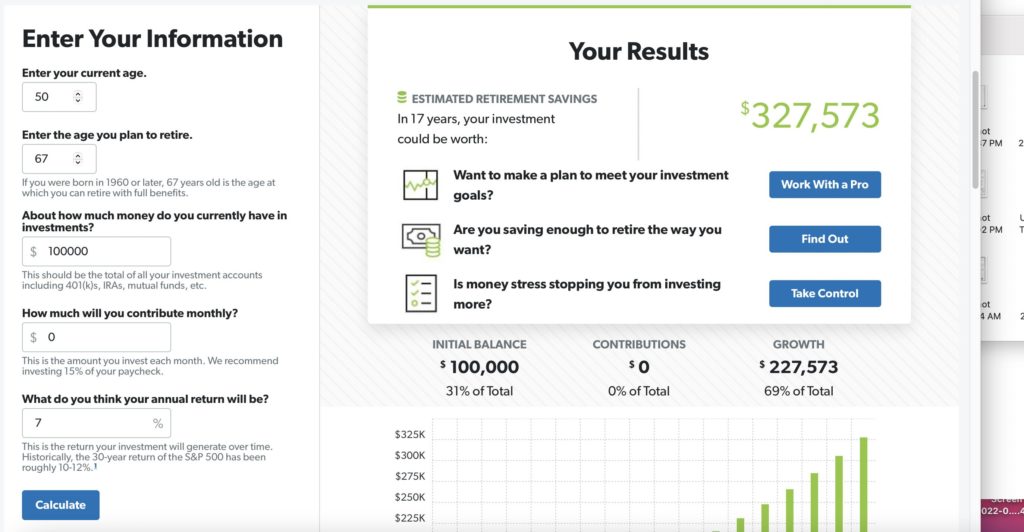

Now, let’s run this same calculation for someone that is age 50 with $100K:

In this scenario, the growth is still impressive at 327K–but it’s nowhere near the power that the 30 year old investor had–the only difference here is time, folks.

Coast FIRE requires there to be ample time for compounding and riding the market ups and downs before arriving at the final destination of full retirement.

Social Security and Coast Fire

People tend to forget this when they run the numbers–but you should honestly factor in some form of social security payment into your numbers.

Let’s be real–none of us know what the future holds for social security–but we ought to assume that there will be something. Be conservative, but include the numbers. It will likely mean that you need less than you think to be on the “Coast Fire” track–probably a lot less–since the government will be kicking you a check every month that will reduce the burn on your asset nest egg.

Why $500K is probably more than enough

$500K in assets in your 30s will most likely qualify you for COAST Fire. Hell, I’d venture to guess that you’re probably COAST FIRE all the way up until at least 45 if you have that much in assets.

Of course, all of this comes down to what your anticipated expenses will be when you full hit retirement, and if you factor in social security payments into the equation at all.

More than likely, you’ll be in good shape with around $1M plus social security payments, which gives you around 10-14 years to let that $500K grow in to your magic number.

Assuming you’re under the age of 50 with that number of assets–you’ll be in good shape going into retirement. If you plan on being a big spender in retirement–well maybe don’t worry about retiring early at all and keep slaving away! (you can tell my sarcasm here).

After Hitting Coast FIRE

Having a paid-for house is a big goal of mine–and something that can help lower the monthly expense dramatically during early retirement.

A lot of so-called financial experts shun the idea of paying off the house–arguing that the money can grow more in an index fund.

That is true in spreadsheet land–but in the real world, stability can be a big thing. With mortgage interest rates above 5%–having a paid for house is like owning a high paying bond, that you can also live in.

If I hit a solid Coast FIRE number like $500K–I’d seriously consider getting the house paid for and accelerating myself toward the full FIRE by lowering my largest monthly expense.